Las 20 mejores soluciones de Core Banking para PYME

El panorama en rápida evolución de la banca digital plantea retos únicos a los bancos pequeños y medianos, obstaculizados por los altos costes y la complejidad de integrar nuevas tecnologías en los sistemas existentes. Obtenga más información sobre los principales retos que plantea el lanzamiento de plataformas bancarias para bancos medianos y pequeños y cómo superarlos. Descubra los 20 principales proveedores de plataformas bancarias básicas.

Autor: Alena Tomchuk

Última actualización el 29 de marzo

Contenido

Introducción

Los bancos pequeños y medianos son importantes en el ámbito de las fintech. En julio de 2023, el valor de las empresas fintech que cotizan en bolsa era de 550.000 millones de dólares. Esto suponía el doble de su valor en 2019.

Estos bancos también desempeñan un papel crucial en el sistema financiero de Estados Unidos. En diciembre de 2022, había 4.001 bancos comunitarios con más de 27.511 sucursales en todo Estados Unidos. Prestan servicio a cerca de 1.400 condados con poblaciones inferiores a 50.000 habitantes, atendiendo a más de 28 millones de personas.

También proporcionan empleo a más de 136.000 trabajadores dentro de sus comunidades y poseen activos por un valor total de 860.000 millones de dólares. Estos datos ponen de relieve cómo los bancos pequeños, medianos y comunitarios contribuyen significativamente tanto al sector de las tecnologías financieras como al panorama financiero en general.

Principales retos

1. Modularidad

La modularidad en la banca digital ayuda mucho a los bancos pequeños y medianos. Les permite probar cosas nuevas y crear productos financieros novedosos con rapidez. Utilizando bien este modelo, los bancos consiguen tres cosas clave que desean: facilidad de uso, capacidad de elección e influencia. De este modo, sólo tardan meses en empezar a ofrecer nuevos servicios. Es más rápido que los sistemas bancarios tradicionales, que tardaban meses y años en crear un producto.

Además, la modularidad convierte a un banco en un lugar donde se venden diferentes herramientas financieras. Esto permite a los bancos ofrecer soluciones únicas y relacionadas con su nicho. En 2022, el valor del mercado de la banca digital superará los 9,4 billones de dólares. Y se espera que crezca a una tasa media de alrededor del 3,6% hasta 2032.

Por lo tanto, si un banco quiere ir por delante de los demás en esta era en la que todo se digitaliza rápidamente, debe tener en cuenta la modularidad. Eso es lo que hace que las plataformas bancarias virtuales sean más elegantes.

2. Orquestación de API

La orquestación de API desempeña un papel importante a la hora de elegir un sistema de banca digital. Permite a los bancos controlar muchos tipos de contactos con los clientes, lo que les permite trabajar sin problemas con otros sistemas. Con esta función automática, los nuevos servicios y productos pueden llegar al mercado más rápidamente.

Las API ayudan a que los dispositivos, las aplicaciones y los datos se conecten mejor. Se están convirtiendo en herramientas cada vez más comunes para las estrategias bancarias dentro y fuera de la empresa. Muchos expertos coinciden en que su importancia ha crecido en los últimos dos años y, según encuestas mundiales, cerca del 88% de los encuestados está de acuerdo con esto.

Además, el 81% considera que las API son cruciales tanto para el trabajo empresarial como para el de TI. Los bancos esperan duplicar el número de API internas de aquí a 2025 junto con las que se utilizan fuera, lo que les ayudará a integrarse también con otros sectores y empresas. Por tanto, podemos decir que la orquestación de API beneficia enormemente a las plataformas de banca digital en términos de velocidad y flexibilidad.

3. Cumplimiento normativo

Cumplir con las normas es realmente importante a la hora de seleccionar una plataforma de banca digital. Mantiene todos los sistemas seguros y actualizados con las normas más recientes. Mediante el uso de la tecnología adecuada, los bancos digitales pueden hacer que sus procesos de cumplimiento sean más fluidos, reducir los errores cometidos por humanos y mantenerse al día con los requisitos reglamentarios. En el ámbito de la banca, el cumplimiento normativo a menudo debe formar parte de las soluciones de software financiero desde el principio.

Los reguladores suelen conceder pocas autorizaciones porque los modelos de negocio bancario basados en Internet aún no están tan maduros ni desarrollados. Sin embargo, en China, los bancos digitales han crecido hasta acaparar el 5% de la cuota de mercado de préstamos al consumo sin garantía. Esto demuestra que seguir bien la normativa es vital para cualquier banco que quiera mantener su buen nombre y seguir siendo competitivo en la era en que todo se hace por Internet.

4. Opciones de personalización

Los bancos pueden utilizar la IA y el big data para adaptar sus servicios a las necesidades específicas de cada cliente. Este enfoque, llamado banca personalizada, puede mejorar significativamente la experiencia que tienen los clientes. También atrae a nuevos clientes.

Presentar una plataforma de banca digital adaptable con funciones de personalización de alto nivel lo hace posible. Estas funciones permiten a los bancos ajustar fácilmente su catálogo de servicios, evitándoles problemas informáticos.

Los estudios muestran que el 89% de los estadounidenses utilizan canales de banca móvil. De ellos, el 70% afirma que ahora accede principalmente a sus cuentas a través del móvil. Añadir personalización a estas plataformas mejora el compromiso con los usuarios y los satisface mejor. Esto reduce las tasas de abandono de clientes y el gasto en conseguir nuevos titulares de cuentas. En resumen, las opciones de personalización hacen que las plataformas de banca digital sean más eficientes y versátiles.

5. Formación y soporte

La formación y el soporte ayudan tanto a los trabajadores como a los clientes a utilizar bien la plataforma. Si los trabajadores tienen una buena formación, pueden utilizar las funciones de la plataforma para hacer mejor su trabajo y ayudar también a los clientes. Un buen servicio de asistencia puede solucionar los problemas con rapidez, lo que hace que el uso del software sea menos frustrante.

Muchos bancos africanos están de acuerdo con esta idea. Una encuesta reveló que el 96% afirmaba que cambiar a la banca digital era fundamental para el plan de crecimiento de su banco. Los bancos medianos podrían alcanzar sus objetivos digitales gastando sólo entre el 20% y el 30% de lo que suele costar una actualización importante del core bancario. En resumen, cuando los bancos quieren sacar el máximo partido de la digitalización, la formación y la asistencia son muy importantes.

6. Coste total de propiedad

Los bancos pequeños y medianos deben tener en cuenta el coste total de propiedad (CTP) a la hora de elegir una plataforma de banca digital. Estos costes pueden provenir de muchas fuentes, como las necesidades tecnológicas, las tasas de software, el almacenamiento de datos, los esfuerzos de seguridad en línea y los salarios del personal. Por ejemplo, la infraestructura tecnológica de las plataformas bancarias digitales puede costar entre 1 y 10 millones de dólares.

La banca digital también puede ser muy útil para las pequeñas empresas. Según el Banco Central Europeo, alrededor del 20% de estas empresas en Europa son las que más dificultades tienen para financiarse. Este problema puede tener una solución más fácil gracias a los servicios simplificados que ofrecen los bancos digitales.

Sin embargo, a la hora de decidir qué plataforma utilizar, los bancos deben tener en cuenta tanto el coste total de propiedad como el rendimiento que podrían obtener de su inversión. Por lo tanto, es importante que los bancos comprendan en qué consisten estos costes totales antes de tomar una decisión.

2. Enhanced Digital Offerings

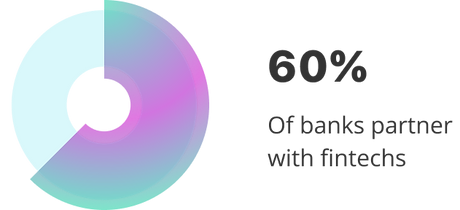

Banks partner with fintech companies because it lets them provide their customers newer, better services. Fintech firms have fresh ideas and easy-to-use designs which can enrich the digital banking experience. or this reason, most banks are now tapping into the power of fintech partners, about six out of ten or 60% according to research findings, for effective digital banking services. They also leverage these collaborations to create custom solutions that fit different customer needs perfectly while keeping up with market trends as it evolves over time.

.png)

3. Improved Customer Experience

Another reason for banks to turn to fintech companies is that they offer cutting-edge technologies and easy-to-use interfaces. Banks aim for a more digital, customer-friendly service with these partnerships. Figures from Gartner highlight that the average bank partners with around 9.4 fintech companies at one time.

Moreover, in 2019 it was reported that around 84% of banks are on the lookout for partnering with new fintech companies aimed at enhancing how they serve customers.

These partnerships provide benefits beyond just improving customer service though; they offer these traditional institutions flexibility as well - so much so that they can meet specific needs of diverse customer groups effectively and keep up with changing consumer demands as well.

4. Backend Infrastructure

Banks play a huge role in helping fintech firms grow. They provide these tech-driven firms with the backend infrastructure they need to thrive. Think of it as a partnership where both parties benefit. For instance, look at how Cross River Bank and Affirm work together.

The bank oversees Affirm financial matters and makes sure it complies with regulations. In return, Cross River gains from the new and innovative ideas that Affirm brings to the table through its buy now, pay later offering.

These successful collaborations pave way for more partnerships called Banking as a Service (BaaS). Experts estimate BaaS will generate massive revenue rates by 2030. It could pull in between $300-$350 billion globally while Europe alone might see earnings between $60-$80 billion by 2025.

In other words, up to one-quarter of all income in banking may come from BaaS offerings over this decade! This is just the beginning of how banks working with fintechs can reshape finance services.

5. Compliance Support

Banks must follow regulations and they also do lots of paperwork. However, fintech companies can help with this. Take for instance, innovative solutions. Fintechs supply these to simplify compliance processes for banks. This results in less costs and confusion for financial institutions.

Some fintech firms go further; they create RegTech solutions to automate tasks, ensuring compliant behavior becomes easier than ever before.

A study shows this is a real need too: According to the study, out of all the respondents working in fintech, 16% of the respondents already use RegTech solutions. Not only that - another 34% say implementing these has altered managing their compliances altogether.

Banks need fintechs because they offer simple ways for banks to fulfill strict laws using technology so they can focus more on satisfying their customers' needs.

6. Brand Reputation

Partnerships between banks and fintechs also reflect the brand image of both of the partners. This type of collaboration brings in many benefits. It leads to wider distribution networks and enhanced product portfolios. Banks can modernize their platforms and make their operations more effective.

A study by PWC in 2019 showed interesting facts about these collaborations. 42% of surveyed banks were actively engaged in partnerships with fintechs. Over time, that number more than doubled to 94%, as more firms showed faith in fintech partnerships for revenue growth.

The trend further reveals that 78% among them have at least 11 or more fintech partners under their fold. This data makes it clear that digital expansion through innovative services is in every bank's benefit.

7. Cost Efficiency

The partnership between fintechs and banks also results in making the services cost effective. Banks leverage tech to become more efficient in their operations. They automate tasks, streamline processes and cut down on mistakes made by humans.

These partnerships bring along advanced data tools as well. These tools offer insights into customer behavior patterns or hidden market trends. This results in better decisions being made, where resources end up where they're needed most, and bank performance gets a boost.

However, there's yet another big win from these collaborations: expansion of banking services. By partnering with fintech solutions, new opportunities of growth and expansion opens up, whereby undeveloped populations get access to crucial financial services while existing customers get products crafted precisely for them.

A perfect case of bank and fintech cooperation was JPMorgan Chase partnering with OnDeck back in 2017. The goal for JPMorgan was to update their small business lending process, using advanced technology from OnDeck. They employed data analytics and this sped up the process.

This new speed was not the only benefit, as the partnership also helped run things smoothly. It used to be hard for small businesses to get loans but that changed with this partnership.

The outcome exceeded expectations - costs went down while better loan decisions were made thanks to helpful insights drawn out by data analytics. This expansion also now meant the availability of more opportunities for small business owners.

Challenges of Partnering with Banks

Dependency on a Single Partner

Fintech companies face constraints tied to a single bank partner. Benefits exist, like managing laws and licenses, but their growth may be limited.

This is because the bank often asks the fintech company to follow risk and compliance practices. That's difficult with a lean structure. Additionally, they're responsible for legal issues connected to their services through the partnership.

Quick innovation poses another challenge due to these regulatory pressures. As of July 2023, publicly traded fintechs have totaled around $550 billion in market value. This shows a large growth potential in this sector.

Limited Flexibility for Product Launches

Another challenge hindering partnership between fintech companies and banks is that partner banks may not be quick enough to support new product launches. Large and complex, these traditional financial institutions have processes that can take time.

In contrast, fintech companies are usually small but fast-moving businesses. They have the capacity to create fresh ideas quickly. But the legacy systems of their banking partners could slow them down. This lack of flexibility challenges how fintechs work best: By innovating and adapting swiftly to market needs.

This also limits space for launching products and is a significant obstacle that hampers these partnerships, which if addressed right, holds great potential in revolutionizing our banking experience!

Geographic Coverage Constraints

Banks that are partnered with fintech companies usually work in one country only. This can limit how far these fintech companies can reach and might even hinder their plans to grow bigger. The reason behind this is the numerous rules and regulations each country's bank has to follow. When a bank tries to operate in another country, it encounters many more complex rules which can be a challenge for any fintech company planning expansion.

Experts predict that the value of all the businesses within fintech could rise up to $882.30 billion by 2030 alone! On the other hand, if partner banks keep preventing fintech from growing beyond borders due to local laws then this predicted growth might face some obstacles.

Operational Challenges

Another challenge banks and fintech companies might face relates to operational challenges when they enter into partnerships. A study points out that 75% of banks find it hard to meet the business needs in such partnerships. Fintechs, too, have their share of challenges meeting high quality standards and using outdated methods set by banks.

Data also becomes a challenge for fintechs. This is because around 81% of fintechs worldwide find it tough to use data for analysis, machine learning, or linking with customer's apps and data systems. These issues may slow down new ideas coming from these partnerships or limit what they can achieve together.

Structural Misalignments

The way banks and fintech startups are run is different. These differences can make creating partnerships hard. Banks use outdated systems which makes it difficult for them to incorporate new, more efficient ways of doing things. New government regulations may also limit their ability to change.

Fintech startups on the other hand value innovative ideas, accept changes easily and quickly introduce new tech solutions. This difference in approach between the two often leads to challenges when they try to work together.

Even so, data shows an interesting trend: As of 2021, it was found that banks often partner with about 2-3 fintech companies in spite of all these difficulties which shows a move towards collaboration between both regardless of challenges faced.

Middleware Technology for Fintechs

Middleware takes care of communicating safely between core banking systems on one end and customer-facing systems on the other. Building a fintech project with a middleware technology allows for greater flexibility in managing the product life cycle. Additionally, the middleware helps facilitate the partner ecosystem and marketplace within a single fintech app.

API stands for Application Programming Interface. In a simple way, it's the part of the server that receives requests and sends responses. The use of both of these tools is highly beneficial for the fintech companies. Some of the benefits of API orchestration and middleware technology are discussed below.

Product Development Opportunities

The use of API orchestration and middleware technology can help financial tech companies in building new products when they work with banks. Based on a study by Velmie, these tools allow different services to be packaged together for customers. This helps a company stand out from its competitors.

These tools also make data sharing easy and provide tailored experiences based on what customers want or need. The good thing about them is that companies can add new services any time they spot changes in customer needs or their own business operations.

This is quite unlike old legacy systems that require total replacement if you need to add new features or services. These legacy systems are also difficult to manage due to their basic technology processes which limit flexibility.

Functional Portability

Another great thing about APIs is that it lets financial tech companies create exactly what the market needs. They help connect different systems together to make personalized solutions that can change when business changes.

A global survey found that around 88% respondents think APIs have become more critical in the past two years, while 81% respondents see it as an important factor for both businesses and IT tasks.

Additionally, data also reveals that the number of open banking API calls is also set to increase to 580 billion in 2027 from 102 billion in 2023, highlighting the use of API’s in financial processes.

Automation and Efficiency

Software tools like API orchestration and middleware can help fintechs to automate tasks, making them more efficient. They can also help manage APIs better, increase safety, and provide more info about how these APIs are functioning.

Separately, middleware technology also connects the main banking system with other platforms that deal with customers directly. This allows information to flow smoothly between them all while saving time and reducing errors.

A study by McKinsey highlights that half of the jobs being done today could be automated between 2030 to 2060. Moreover, it was also reported separately that about 64% of people around the world used at least one app from a fintech company in the year 2022. This number was two times larger than what it was five years ago. This shows how important and impactful automation is becoming in the field of finance technology.

Increased Security

API orchestration and middleware technology can also help make baking procedures safe. These kinds of technologies let you manage, control, and watch over APIs better which makes it harder for online threats to breach into the systems.

With rising cyber threats worldwide, fintech companies are focusing more on cybersecurity. A recent study shows almost 84% of leaders in fintechs plan to invest more in IT safety measures like identity authentication within the coming years.

Another report showed a huge increase - about 742% every year on average - in attacks on software supply chains for three years straight. All this just further strengthens how important raising security is through use of API orchestration and middleware technology specially for fintech's.

Las 20 mejores plataformas bancarias básicas para PYME

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

(Reino Unido) ClearBank se construyó con la creencia de que la infraestructura bancaria ya no frenaría el progreso. Más bien, sería el catalizador que libera el potencial para innovar. Se adaptaría para atender diferentes necesidades y así comenzar una nueva era en los servicios financieros.

Conclusion

In conclusion, fintech companies and banks working together is something that benefits both parties. It allows each one to benefit from the other's strong points. Banks provide fintechs important tools they need like backend infrastructure, regulatory expertise, and compliance frameworks while fintechs help banks grow bigger, come up with new innovative ideas and make customers happier.

Still, these partnerships come with its own set of challenges. Often, a fintech company can find itself limited because it gets tied down to one bank. Launching new goods or services becomes harder when partner banks don't offer necessary support.

You might also be interested in

Obtenga información útil de expertos de la industria sobre las tendencias del mercado Fintech en 2024

Partner banks also usually only work in one country which restricts collaboration opportunities.

Yet there are solutions for these challenges like implementing middleware technology including API orchestration that acts as mediator between fintech and its partner bank by simplifying communications between them.

As we look ahead to 2024, several top partner banks in the USA stand out for their commitment to innovation and collaboration. These institutions continue to foster an ecosystem where fintechs thrive, creating a win-win scenario for the financial industry and its customers.